Speedread

Virtus is listing two new ETFs: a BDC ETF, in an attempt to underprice VanEck; and an MLP ETF

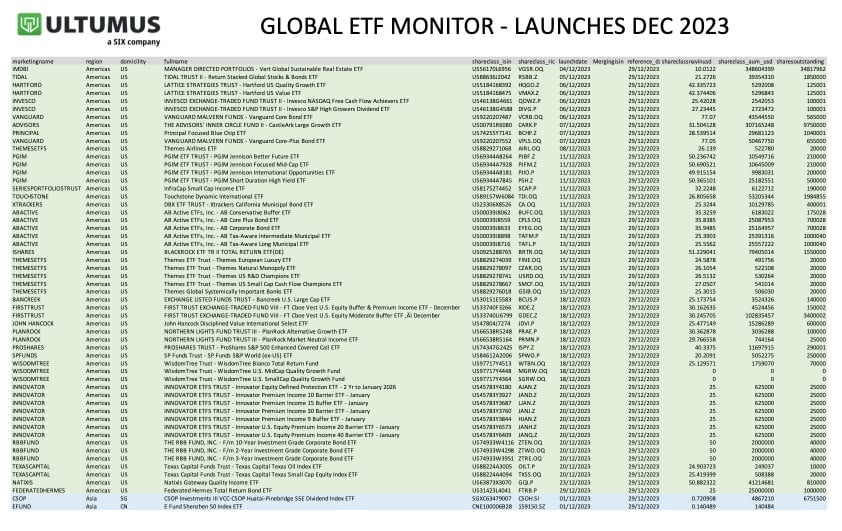

USA

Virtus lists MLP, BDC ETFs

- Virtus Private Credit Strategy ETF (VPC)

- Virtus Real Asset Income ETF (VRAI)

What is a BDC?

BDCs are a confusing hodgepodge. They look like REITs because by law they have to distribute 90% of their income as dividends. But they smell like private equity because they typically invest in the equity and debt of mid-sized US firms. Most of what they do is make loans, typically to companies that are deemed too risky for banks. This can be great, because they often yield 8 – 12%. But can mean real risk and huge drawdowns in bear markets.

Why are the fees so ridiculously high?

The prospectus indicates that the fund will be charging a 7.6% annual fee, making it perhaps the second most expensive ETF in the world. (VanEck’s BIZD, the first ETF to start investing in BDCs and most expensive ETF in the world, charges an even higher fee of 9.4%.)

The fee is so high because it includes the fees of the underlying BDCs. SEC rules require fund-of-funds to enumerate their total fees in the prospectus expense table. (VanEck's education piece is available here.)

The MLP ETF

The Virtus Real Asset Income ETF (VRAI) will invest in other alternative assets that produce income.

These include more familiar items like REITs and overseas companies. As well as MLPs, which are trusts that invest in natural resource infrastructure like gas pipes. (They are typically high yielding. This is because they are trusts/partnerships -- not corporations. And therefore do not have to pay corporate tax.) As is often the case for ETFs that invest in MLPs, the holdings of MLps is limited to 20% of NAV, due to tax law reasons. Almost all MLPs are based in Texas.

The fund will charge 0.55%.